Understanding how a home equity credit loan works is essential if you're considering taking out one. This type can be secured by your home. It comes with a fixed repayment period, as well as an interest rate. You must own your home and have equity. This means that the total amount you owe on your home must be less than the market value of your house. To determine if you're a good candidate, your lender will also look at your credit score and debt to income ratio.

Revolving credit secured by your home

A home equity line of credit, or HELOC, is a revolving line of credit from a lender that enables you to borrow against the equity in your home. This type of credit can be used for large-scale debt consolidation or to pay off high-interest bills. You can also deduct the interest from these loans.

A home equity line credit is only available to homeowners who have equity in their homes. You must have a lower total amount than your home's market value. Lenders also evaluate your credit score, debt-to-income ratio and payment history.

A home equity line credit can help with major expenses such medical bills, home repairs, and education. Although a line of credit can be used to cover monthly expenses, you should also understand the risks. You should have an emergency fund in place for when you borrow more than you can pay back.

Repayment period

The amount of the loan and equity in the home will determine the repayment period of a home equity credit line. While the maximum loan amount for all borrowers is the same, the repayment term will vary depending upon the total loan amount and how much equity the home has. Quick calculations can help you calculate the repayment time for a HELOC.

The repayment period for a home-equity line of credit has two phases. The first is the draw period, which usually lasts 10 to 15 years. You'll be making payments on the principal and interest of the credit line during this time. The second phase is the repayment period, which begins once the draw period ends.

There are different repayment periods for a home equity credit line. For example, a HELOC may allow you to make interest-only payments during the draw period, and a home equity payment plan may allow you to make principal-and-interest payments after the draw period. This will reduce your monthly payments.

Interest rate

A home equity line credit's interest rate can be variable. The margin depends on many factors such as the loan-to-value ratio, credit qualification, property state, and other factors. Typically, the interest rates are lower when the loan first opens, but can increase over time.

The maximum amount you can borrow for a home equity line credit is dependent on your home's current value, the proportion of your home equity that you owe, and your income. You can get an idea of how much you could borrow by doing a simple calculation. You could borrow as much as $20,000. If you owe half of the home's worth, for example.

While the five-year home equity loan of credit interest rates are competitive with other rates, it's important to note that a longer repayment term (five years) will result in a lower interest rate, but you'll have to make a larger monthly payment. Rates vary depending on credit scores. However, the rates that are available to qualified borrowers with a loan ratio of 80% or more will generally be the lowest. Credit scores of 740 and higher are required in order to qualify.

FAQ

Is it possible to quickly sell a house?

If you plan to move out of your current residence within the next few months, it may be possible to sell your house quickly. You should be aware of some things before you make this move. First, you must find a buyer and make a contract. Second, you need to prepare your house for sale. Third, your property must be advertised. Lastly, you must accept any offers you receive.

What are the pros and cons of a fixed-rate loan?

Fixed-rate mortgages lock you in to the same interest rate for the entire term of your loan. This means that you won't have to worry about rising rates. Fixed-rate loans also come with lower payments because they're locked in for a set term.

Do I need flood insurance

Flood Insurance covers flooding-related damages. Flood insurance can protect your belongings as well as your mortgage payments. Learn more information about flood insurance.

Can I get another mortgage?

However, it is advisable to seek professional advice before deciding whether to get one. A second mortgage is usually used to consolidate existing debts and to finance home improvements.

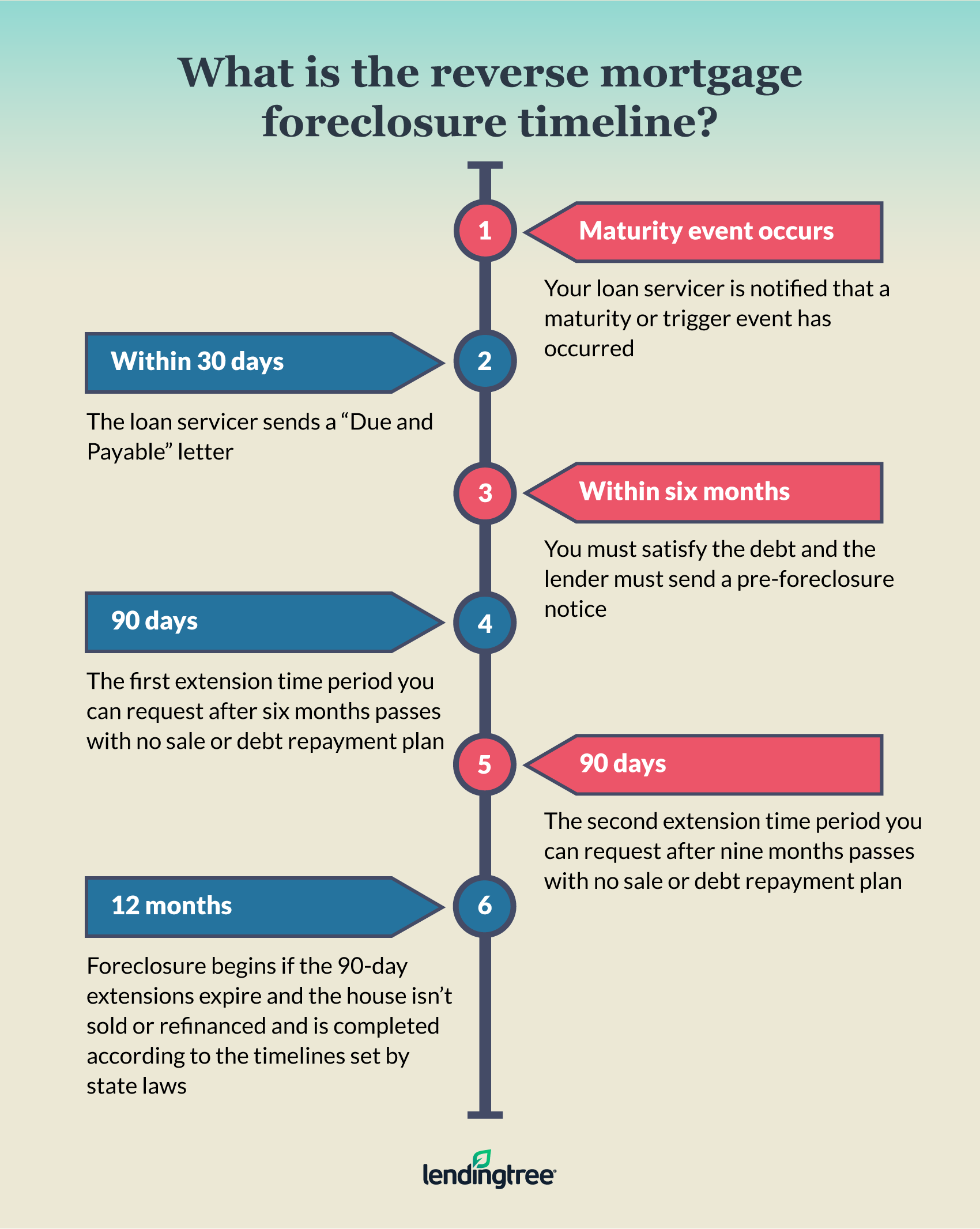

What is reverse mortgage?

A reverse mortgage lets you borrow money directly from your home. You can draw money from your home equity, while you live in the property. There are two types of reverse mortgages: the government-insured FHA and the conventional. A conventional reverse mortgage requires that you repay the entire amount borrowed, plus an origination fee. FHA insurance will cover the repayment.

How much does it cost to replace windows?

Replacing windows costs between $1,500-$3,000 per window. The total cost of replacing all of your windows will depend on the exact size, style, and brand of windows you choose.

Statistics

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

External Links

How To

How to locate an apartment

The first step in moving to a new location is to find an apartment. Planning and research are necessary for this process. This involves researching and planning for the best neighborhood. While there are many options, some methods are easier than others. These are the steps to follow before you rent an apartment.

-

Data can be collected offline or online for research into neighborhoods. Websites such as Yelp. Zillow. Trulia.com and Realtor.com are some examples of online resources. Online sources include local newspapers and real estate agents as well as landlords and friends.

-

You can read reviews about the neighborhood you'd like to live. Yelp, TripAdvisor and Amazon provide detailed reviews of houses and apartments. You might also be able to read local newspaper articles or visit your local library.

-

Make phone calls to get additional information about the area and talk to people who have lived there. Ask them what they liked and didn't like about the place. Ask them if they have any recommendations on good places to live.

-

You should consider the rent costs in the area you are interested. Consider renting somewhere that is less expensive if food is your main concern. If you are looking to spend a lot on entertainment, then consider moving to a more expensive area.

-

Learn more about the apartment community you are interested in. It's size, for example. What is the cost of it? Is it pet-friendly? What amenities does it offer? Are you able to park in the vicinity? Are there any special rules that apply to tenants?