A refinance allows you to borrow money against the equity of your home. For borrowers who have additional cash but are unable to pay the full amount, a home equity loan may be an option. Although both options are viable, cash-out refinances can be smart for homeowners with equity in the home. Although cash-out refinances are more affordable and easier to qualify for than other options, they can also be expensive.

Refinances that cash out have lower interest rates

Cash-out refinances are a great way to get the most out of your home's equity, without spending as much on it as you would with a home equity mortgage. This loan has its drawbacks, however. Cash-out refinances can make your mortgage more expensive, extend your repayment period, and even increase your risk of foreclosure.

While cash-out refinances usually have lower interest rates that home equity loans, you will still need to pay fees. Closing fees can amount to up to 3 percent of the new mortgage. Property taxes and homeowners insurance are also required. You may find cash out refinances a great option if you have good credit.

They are easier to qualify for

A home equity loan is a loan that allows a homeowner to borrow against the equity in their home. These loans have lower interest rates, and are easier to obtain than a mortgage refinance. A home equity loan may also have a lower closing cost and be more flexible than a traditional mortgage. It is important that you understand the requirements before applying for a home equity mortgage.

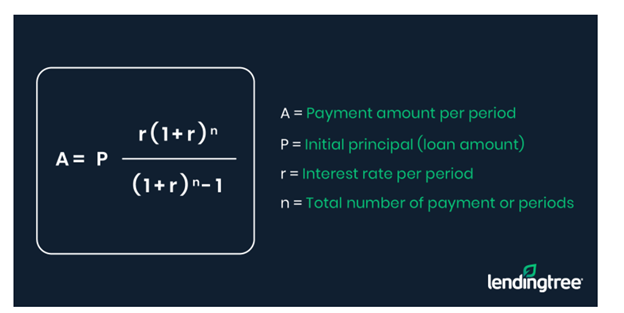

A home equity loan lets you borrow against the equity in your house and then repay it in an agreed amount of installments that includes interest and any fees. This loan is also known by the name "second mortgage" because it borrows against your home and then pays back in a set amount of installments, which includes interest and fees. If you default on the loan the lender can foreclose your home. While refinancing is more common than a mortgage to fund your home equity, it's important to evaluate all factors before choosing a loan.

They are more convenient

A home equity loan may be an option if you have excellent credit and substantial equity in your home. You may also be able to benefit from a cash out refinance if your monthly mortgage payment is low. You should get multiple quotes from different lenders before you finalize your decision. A detailed list of fees for lending should be requested.

Refinance is a loan to replace your existing mortgage. A home equity mortgage, on the other side, is a second loan which you take out in addition to your current mortgage. Both have their pros and cons. Before you decide which one is best for your needs, it is important that you fully understand the risks associated with each.

They are more expensive

A refinance loan can save you money in the long run because it will allow you to release the equity in your home. Refinance loans are more expensive upfront but will have lower monthly payments than home equity loans. A home equity loan will still be affordable if your goal is to repay the loan in six or less months.

A home equity loan is much simpler to obtain. The closing costs will still be payable. These costs are typically not tax-deductible. Flexibility is another advantage to a home equity loan. The money can also be used to finance large purchases or pay for other major expenses.

FAQ

What are some of the disadvantages of a fixed mortgage rate?

Fixed-rate loans have higher initial fees than adjustable-rate ones. Additionally, if you decide not to sell your home by the end of the term you could lose a substantial amount due to the difference between your sale price and the outstanding balance.

What's the time frame to get a loan approved?

It depends on many factors like credit score, income, type of loan, etc. Generally speaking, it takes around 30 days to get a mortgage approved.

How can I determine if my home is worth it?

You may have an asking price too low because your home was not priced correctly. If you have an asking price well below market value, then there may not be enough interest in your home. Get our free Home Value Report and learn more about the market.

How do I eliminate termites and other pests?

Termites and other pests will eat away at your home over time. They can cause serious destruction to wooden structures like decks and furniture. To prevent this from happening, make sure to hire a professional pest control company to inspect your home regularly.

Statistics

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

External Links

How To

How to Find an Apartment

The first step in moving to a new location is to find an apartment. This process requires research and planning. This involves researching and planning for the best neighborhood. While there are many options, some methods are easier than others. Before you rent an apartment, consider these steps.

-

It is possible to gather data offline and online when researching neighborhoods. Online resources include Yelp. Zillow. Trulia. Realtor.com. Offline sources include local newspapers, real estate agents, landlords, friends, neighbors, and social media.

-

Read reviews of the area you want to live in. Yelp. TripAdvisor. Amazon.com all have detailed reviews on houses and apartments. You may also read local newspaper articles and check out your local library.

-

Call the local residents to find out more about the area. Talk to those who have lived there. Ask them about what they liked or didn't like about the area. Ask if they have any suggestions for great places to live.

-

You should consider the rent costs in the area you are interested. If you think you'll spend most of your money on food, consider renting somewhere cheaper. Consider moving to a higher-end location if you expect to spend a lot money on entertainment.

-

Find out about the apartment complex you'd like to move in. How big is the apartment complex? What is the cost of it? Is it pet friendly? What amenities are there? Can you park near it or do you need to have parking? Are there any special rules that apply to tenants?