Reverse mortgages allow you to borrow against your equity. Your equity is simply the difference between your home's appraised value and the amount you owe for the mortgage. As your home becomes more valuable, your equity will also increase. The lowest-cost type of reverse mortgage is the Single-Purpose reverse mortgage. These loans don't have strict eligibility requirements. Interest rates are also low.

Private reverse mortgages have no strict eligibility requirements

Home equity conversion mortgages are the most common type of reverse mortgage. They are insured by the Federal Housing Administration and are subject to strict eligibility requirements. To be eligible, home-owners must be at the age of 62 and have less than $150,000 in mortgage debt. HECMs are available as lump sum payments, monthly payments, or as a line of credit.

Reverse mortgage borrowers need not make monthly payments on principal, but must still cover recurring housing costs. These expenses can include homeowners insurance premiums or property taxes. Most reverse mortgage agreements require that borrowers pay current property taxes. Lenders may terminate the loan agreement if borrowers fail to pay these taxes. In this case, they will need to repay the balance.

One-purpose reverse mortgages are among the most affordable of the three options.

One-purpose reverse mortgages are typically the most affordable of the three. They are not always available. They are often only available through local and state governments, nonprofit organizations, as well credit unions. To find the best lender, you need to do your homework. Compare the information that you get from each lender and avoid high-pressure sales tactics or hidden fees.

Reverse mortgages can be used for one purpose and are available in different terms. These loans do not have to be repaid monthly, which is a difference from other types of reverse mortgages. The only way these loans can become due is if the borrower stops making payments on homeowners insurance, or if the city condemns your property. The amount of money you can borrow is dependent on your age, the value of your property and other factors. Additionally, you have the option to opt for the term option. This allows cash advances to be made monthly for a certain period.

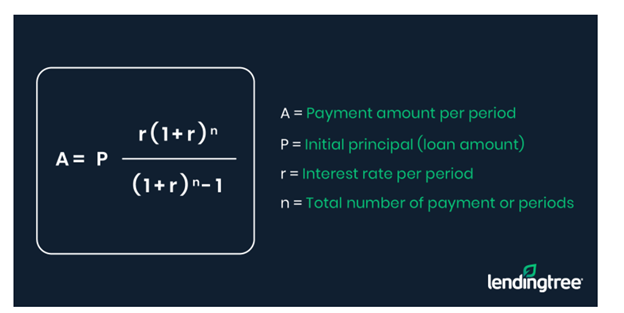

Interest rates

The interest rates for reverse mortgages vary depending on who is lending them. Some offer fixed rates and some have variable rates. Although fixed rate reverse mortgages are more attractive than variable rate options, they will pay you an initial payment that is higher than variable rate. However, rates may change over the years. The average interest rate for a HECM is 5.060%, according to the National Reverse Mortgage Lenders Association. Variable rate reverse Mortgages will fluctuate based upon the market index. Please check with your lender about the current rates.

Variable rate reverse mortgage rates will fluctuate due to external factors. Therefore, the rate that you pay could change each year. This is ideal if you only plan on using the funds once in a while. This type of loan also offers protection against rate hikes as it can only rise by 2% every year. The maximum interest rate increase over the life of the loan is typically 5%.

Reverse Mortgages: Get money

Reverse mortgages are available to people in retirement who need to access a lump sum of money. These loans can be combined with a credit line, which allows the borrower access to the full amount at once. These loans can be more expensive than either monthly payments or line-of credit options. Additionally, they are more risky for younger borrowers.

Those who are in the process of getting a reverse mortgage should be wary of any salesperson who tries to rush the process. These salespeople might push you to sign a contract and/or take a lumpsum payment. It is always better to do your homework and find a reverse-mortgage counselor you feel comfortable working with.

FAQ

What should I look out for in a mortgage broker

A mortgage broker is someone who helps people who are not eligible for traditional loans. They search through lenders to find the right deal for their clients. Some brokers charge a fee for this service. Others provide free services.

How can I determine if my home is worth it?

It could be that your home has been priced incorrectly if you ask for a low asking price. If your asking price is significantly below the market value, there might not be enough interest. Get our free Home Value Report and learn more about the market.

What are the downsides to a fixed-rate loan?

Fixed-rate loans have higher initial fees than adjustable-rate ones. Also, if you decide to sell your home before the end of the term, you may face a steep loss due to the difference between the sale price and the outstanding balance.

Statistics

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

External Links

How To

How do you find an apartment?

Finding an apartment is the first step when moving into a new city. This involves planning and research. It includes finding the right neighborhood, researching neighborhoods, reading reviews, and making phone calls. While there are many options, some methods are easier than others. Before you rent an apartment, consider these steps.

-

You can gather data offline as well as online to research your neighborhood. Websites such as Yelp. Zillow. Trulia.com and Realtor.com are some examples of online resources. Offline sources include local newspapers, real estate agents, landlords, friends, neighbors, and social media.

-

Read reviews of the area you want to live in. Yelp, TripAdvisor and Amazon provide detailed reviews of houses and apartments. You can also check out the local library and read articles in local newspapers.

-

Make phone calls to get additional information about the area and talk to people who have lived there. Ask them about what they liked or didn't like about the area. Ask them if they have any recommendations on good places to live.

-

Take into account the rent prices in areas you are interested in. If you are concerned about how much you will spend on food, you might want to rent somewhere cheaper. Consider moving to a higher-end location if you expect to spend a lot money on entertainment.

-

Learn more about the apartment community you are interested in. It's size, for example. What is the cost of it? Is it pet-friendly? What amenities does it offer? Do you need parking, or can you park nearby? Are there any special rules that apply to tenants?