Investing in properties with tax liens has its benefits and drawbacks. It is essential to learn about the property's costs, requirements, and drawbacks before investing. This article will also cover the ways you can invest in properties that have tax liens. Before you buy a property that has a tax lien, it is important to know its address as well as its owner. This information can be found online.

The drawbacks of investing with tax liens

While tax liens are an attractive option for long-term investing, they also carry some risk. Investors should avoid properties that are subject to delinquent taxes or environmental damage, which could jeopardize their ownership rights. To avoid these pitfalls, investors should research the liens against the property and recent sales of comparable properties. Additionally, investors should verify whether there are any other liens against the property. This could make it more difficult to acquire the property in foreclosure.

The cost of tax lien certificates is another problem. Tax liens can vary in price depending on the property. They are therefore not suitable for short-term investment. Tax liens should not be used by novice investors as they require extensive knowledge of real estate and experience. They are also known to be risky investments so it is important to do thorough research and due diligence.

Cost to invest in property with a tax lien

There are many factors that influence the cost of property investments with a tax lien. It is essential to do extensive research before investing in any property. While tax liens can be a great way of making a profit from real estate, it is important to do your research correctly. The best way of maximising your profits is investing in a property that is financially sound. A good location and neighborhood are also important.

The first step in buying a tax lien is to learn more about real estate law. This will help you to understand the process and protect yourself. There are many laws that apply to the purchase tax liens. You should consult a realty attorney for guidance.

Investment in property subject to a tax lien

You can gain exposure to real estate by investing in property with a tax lien. It is risky and may not suit all investors. While this investment may have its benefits, it is best to only attempt it if you are an experienced investor with extensive knowledge of the property markets.

It is essential to learn as much information as you can about the property before investing. This includes surrounding areas and any other liens which may be affecting your property. Understand the different deadlines and timelines to foreclose.

Methods of investing in a property with a tax lien

Tax lien investing is a win-win situation for the taxing authority and the investor. The taxing authority gets to collect more money and the investor gets a property to own. Tax liens are published in the local newspaper. Investors have the option to bid on the lien at an online auction. It may take several months to complete the process of foreclosing on a property. The investor must be able to afford legal counsel and filing fees during this period. The investor will need to wait several months, or even years before seeing any returns on his investment.

Tax lien investing can be risky and investors should do their homework on all properties. Investing in a property with a tax lien is not a good idea if the property has other liens or has been dilapidated for a long time. A dilapidated property could also have environmental issues.

FAQ

What is reverse mortgage?

Reverse mortgages allow you to borrow money without having to place any equity in your property. This reverse mortgage allows you to take out funds from your home's equity and still live there. There are two types: conventional and government-insured (FHA). Conventional reverse mortgages require you to repay the loan amount plus an origination charge. FHA insurance covers the repayment.

Is it possible for a house to be sold quickly?

It might be possible to sell your house quickly, if your goal is to move out within the next few month. Before you sell your house, however, there are a few things that you should remember. You must first find a buyer to negotiate a contract. Second, prepare the house for sale. Third, your property must be advertised. Finally, you should accept any offers made to your property.

What should I do before I purchase a house in my area?

It all depends on how long your plan to stay there. If you want to stay for at least five years, you must start saving now. But if you are planning to move after just two years, then you don't have to worry too much about it.

How can I determine if my home is worth it?

It could be that your home has been priced incorrectly if you ask for a low asking price. If you have an asking price well below market value, then there may not be enough interest in your home. Our free Home Value Report will provide you with information about current market conditions.

What are the top three factors in buying a home?

Location, price and size are the three most important aspects to consider when purchasing any type of home. Location is the location you choose to live. Price refers how much you're willing or able to pay to purchase the property. Size is the amount of space you require.

What's the time frame to get a loan approved?

It depends on many factors like credit score, income, type of loan, etc. It typically takes 30 days for a mortgage to be approved.

Statistics

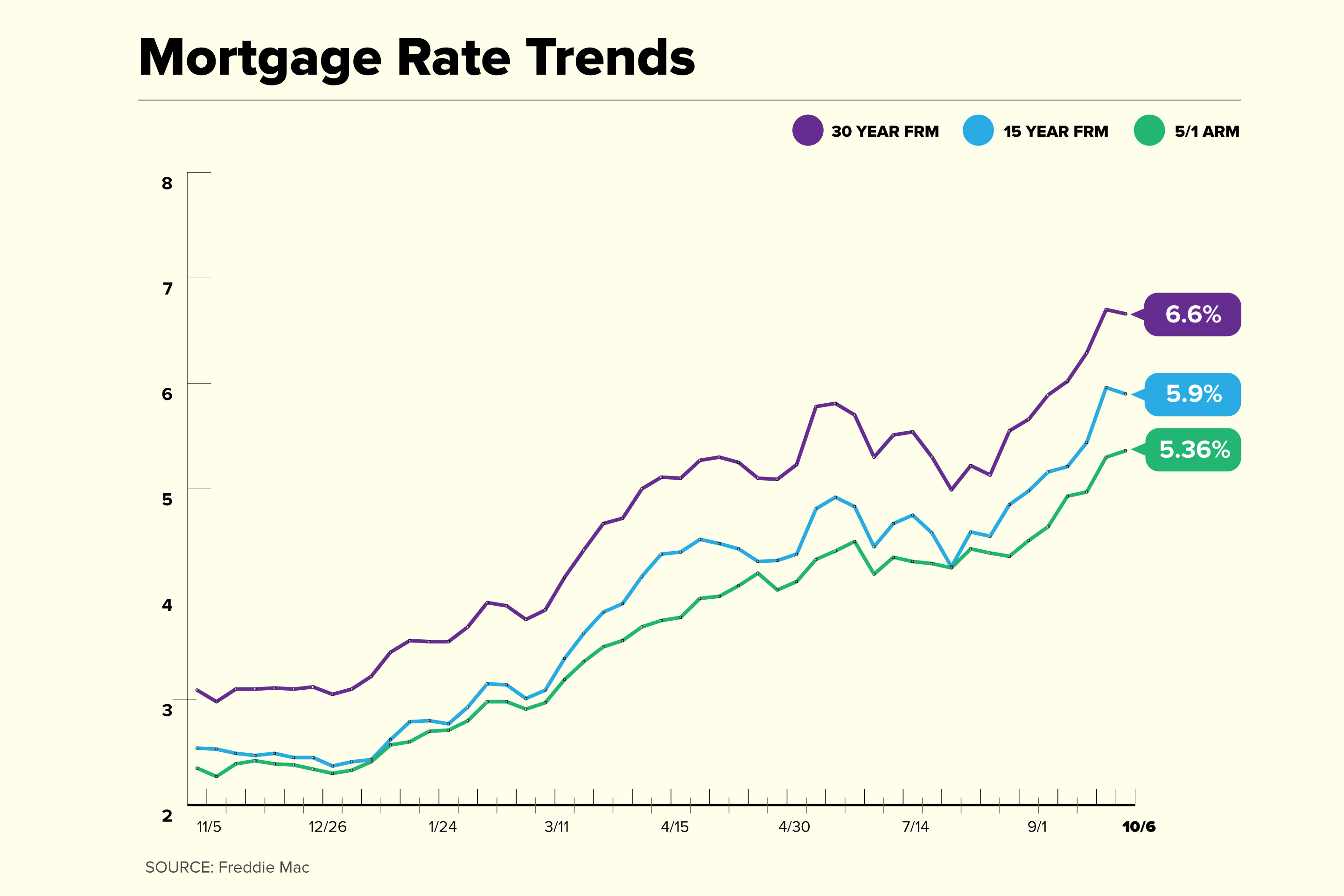

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

External Links

How To

How to purchase a mobile home

Mobile homes are houses constructed on wheels and towed behind a vehicle. They were first used by soldiers after they lost their homes during World War II. People who live far from the city can also use mobile homes. These houses are available in many sizes. Some houses are small while others can hold multiple families. There are even some tiny ones designed just for pets!

There are two main types of mobile homes. The first type is manufactured at factories where workers assemble them piece by piece. This occurs before delivery to customers. You could also make your own mobile home. You'll need to decide what size you want and whether it should include electricity, plumbing, or a kitchen stove. You will need to make sure you have the right materials for building the house. You will need permits to build your home.

These are the three main things you need to consider when buying a mobile-home. Because you won't always be able to access a garage, you might consider choosing a model with more space. A model with more living space might be a better choice if you intend to move into your new home right away. You'll also want to inspect the trailer. If any part of the frame is damaged, it could cause problems later.

It is important to know your budget before buying a mobile house. It's important to compare prices among various manufacturers and models. It is important to inspect the condition of trailers. While many dealers offer financing options for their customers, the interest rates charged by lenders can vary widely depending on which lender they are.

An alternative to buying a mobile residence is renting one. Renting allows the freedom to test drive one model before you commit. Renting is not cheap. Most renters pay around $300 per month.