This article will explain how to calculate PMI for tax purposes. PMI can be used to insure your mortgage. It is tax-deductible. The percentage of the loan amount will determine how much you pay. This means that your monthly payment will depend on how much the loan amount is. The mortgage insurance must be canceled when the loan balance exceeds 78% of its original value. This usually occurs around 12 years.

Private, tax-deductible mortgage insurance

Private mortgage insurance which is tax-deductible can be a type or insurance that is paid by the borrower. This type is generally affordable and plays an essential role in the mortgage lending system. With interest rates rising and home prices slowing, homeowners are paying more for monthly home loans, but PrivateMI can help keep mortgage payments down by protecting against loss. Moreover, it is a tax-deductible expense that the borrower can cancel when they have enough equity in their home.

The federal government extended until 2020 the mortgage insurance premium deduction available to borrowers. But it is important to note that this deduction only applies to private mortgage insurance premiums. It is not available for cash out refinances or home equity loan. To qualify for this deduction, a borrower must itemize their taxes and have income below the phase-out threshold. For mortgages that have been in existence for over three years, borrowers typically pay premiums for mortgage insurance.

LTV

If you've been wondering how PMI is calculated, there are a few things to keep in mind. First, your loan-to value ratio (or LTV) determines how much PMI you will have to pay. LTV is the sum of the loan amount and the value of the home. If this ratio is too high, the lender will deny your application. In such a situation, the lender might request a broker's price opinion (BPO), to confirm the current market value and calculate LTV. You can also request that PMI be stopped early. BPOs or appraisals are usually performed at your expense. However you could save hundreds of money if your mortgage insurance is terminated early.

Your down payment is also a factor in determining the LTV. A down payment of 10% equals a 90% LTV ratio. If you have a 10% downpayment, you will need at least 80% to avoid PMI. To avoid paying PMI, your mortgage must not exceed 80% of the original purchase cost.

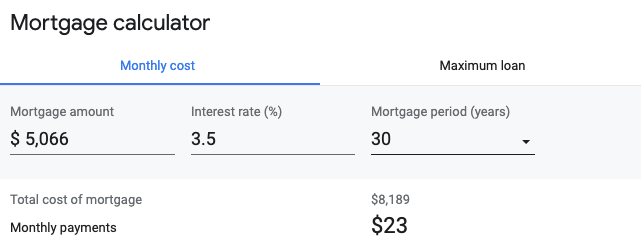

Calculating the PMI

The data from soil chemistry can be used for the calculation of the PMI. These analyses can be used in medical-legal cases and in humanitarian recovery. The accuracy of the result depends on the confidence intervals, which should be within 95% of the nominal value. You must consider the cause of deaths, coverage proportion, as well as the confidence interval to ensure accuracy.

PMI is an extra insurance. It's required for borrowers that don't have enough money to pay all the costs of the loan. Depending on the loan-to-value ratio, this additional insurance can lower the risk for some mortgages.

Get Rid of Paying PMI

There are several ways to get out of paying PMI on a mortgage. One way is to reduce the loan-to-value ratio to less than 80 percent. To do this you will need make timely payments on your loan and prove that there aren't any other liens on the house. The Homeowners Protection Act, (HPA), also contains information about how to cancel PMI.

Another option is to make a minimum 20% down payment. You can also avoid PMI for a longer time. These methods may be easier than others but it can take a long time to complete.

FAQ

How can I determine if my home is worth it?

You may have an asking price too low because your home was not priced correctly. Your asking price should be well below the market value to ensure that there is enough interest in your property. Get our free Home Value Report and learn more about the market.

Can I get a second mortgage?

However, it is advisable to seek professional advice before deciding whether to get one. A second mortgage is used to consolidate or fund home improvements.

How much money do I need to save before buying a home?

It depends on the length of your stay. If you want to stay for at least five years, you must start saving now. But if you are planning to move after just two years, then you don't have to worry too much about it.

How many times may I refinance my home mortgage?

This will depend on whether you are refinancing through another lender or a mortgage broker. Refinances are usually allowed once every five years in both cases.

How much will it cost to replace windows

Replacing windows costs between $1,500-$3,000 per window. The exact size, style, brand, and cost of all windows replacement will vary depending on what you choose.

How do you calculate your interest rate?

Market conditions influence the market and interest rates can change daily. In the last week, the average interest rate was 4.39%. To calculate your interest rate, multiply the number of years you will be financing by the interest rate. Example: You finance $200,000 in 20 years, at 5% per month, and your interest rate is 0.05 x 20.1%. This equals ten bases points.

What are the three most important factors when buying a house?

The three most important factors when buying any type of home are location, price, and size. Location refers to where you want to live. Price is the price you're willing pay for the property. Size refers to how much space you need.

Statistics

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

External Links

How To

How do I find an apartment?

When you move to a city, finding an apartment is the first thing that you should do. This involves planning and research. This involves researching neighborhoods, looking at reviews and calling people. Although there are many ways to do it, some are easier than others. Before renting an apartment, it is important to consider the following.

-

It is possible to gather data offline and online when researching neighborhoods. Online resources include Yelp. Zillow. Trulia. Realtor.com. Other sources of information include local newspapers, landlords, agents in real estate, friends, neighbors and social media.

-

See reviews about the place you are interested in moving to. Yelp and TripAdvisor review houses. Amazon and Amazon also have detailed reviews. Local newspaper articles can be found in the library.

-

Call the local residents to find out more about the area. Talk to those who have lived there. Ask them what the best and worst things about the area. Ask for recommendations of good places to stay.

-

You should consider the rent costs in the area you are interested. If you think you'll spend most of your money on food, consider renting somewhere cheaper. If you are looking to spend a lot on entertainment, then consider moving to a more expensive area.

-

Find out about the apartment complex you'd like to move in. How big is the apartment complex? What is the cost of it? Is it pet friendly What amenities does it have? Is it possible to park close by? Do tenants have to follow any rules?