Mortgage rates for 5/1 ARMs depend on the margin, which is the difference between the interest rate you are paying and the index rate. The index rate fluctuates over time, but the margin is typically set at the start of the loan term and remains unchanged during the life of the loan. The margin is the lower, so you'll pay less interest over the term of your loan.

15-year fixed vs. 5-year ARM

If you are shopping for a home loan, you should know the difference between 15-year fixed vs 5/1 adjustable-rate mortgage (ARM) rates. While the two types of mortgages have some similarities, there are some differences that are worth considering. A 15 year fixed-rate mortgage will have one fixed payment throughout its term. An ARM, on the other hand, will adjust its interest rates based upon the mortgage document. This means that your payment will change with the index value. Fixed-rate mortgages are more expensive than ARMs because they have a shorter tenure.

Five-year adjustable rate mortgage rates are more expensive than 15-year fixed rate mortgages. This is due partly to the fact that five-year ARM interest rates have fallen since mid-2000s. In 2006 the average 5/1 AARM rate was 6.8%. In 2010, the rate was 3.822%. The 15-year fixed mortgage rate is now 5.90%. There is a 0.1 point down payment. Contrast this, the 5/1ARM now stands at 5.90% with a 0.1% down payment.

Interest rate caps for 5/1 ARMs

The interest rate caps for 5/1ARMs restrict how much the interest rates can increase over the course of the loan. The index, the interest rate for the first year and the margin are all affected by the caps. In some cases, they are increased every year or every two years. In some cases they will increase every five year.

In certain cases, the cap might not be applied to initial interest rate. The introductory interest rate is lower than the rate that would apply if the loan were a fixed-rate mortgage. In many cases, the initial rate is one percentage point lower than that which would be applicable at the end of the fixed five-year period. However, once the fixed-rate period is over, the interest rate may be much higher than the initial rate. Most ARMs have an interest rate cap to prevent this. It can be either a monthly cap or a lifetime cap that limits the interest rate rise over the loan's life.

Monthly payments can be kept affordable by using 5/1 ARMs with interest rate caps. The monthly payment is affected by the interest rate. You should ensure that the interest rate caps apply to your particular situation.

Cost of 5/1 ARM loan

The potential consequences of taking out an ARM 5/1 loan should be considered. You will be charged an interest rate which adjusts to market indexes when you take out this type of loan. These mortgages also include caps that limit the amount of interest rate increases. The first cap restricts the rate increase that the loan can make during the first one year. The periodic cap caps how much the rate may rise each time the loan is modified.

The 5/1 ARM loan has a very low initial interest rate, which makes it attractive for those who are looking to buy a home. However, the rate is only fixed over five years. It then adjusts based upon the prevailing interest rate plus any margin. As a result, this type of mortgage is currently being phased out by the financial sector. The process started in the last year, and will continue until lenders stop offering this type of loan. Changes in financial indexes are one reason for the phaseout.

FAQ

What should you consider when investing in real estate?

You must first ensure you have enough funds to invest in property. You can borrow money from a bank or financial institution if you don't have enough money. It is also important to ensure that you do not get into debt. You may find yourself in defaulting on your loan.

You should also know how much you are allowed to spend each month on investment properties. This amount must cover all expenses related to owning the property, including mortgage payments, taxes, insurance, and maintenance costs.

Finally, ensure the safety of your area before you buy an investment property. It would be best if you lived elsewhere while looking at properties.

How long does it take for a mortgage to be approved?

It depends on many factors like credit score, income, type of loan, etc. It typically takes 30 days for a mortgage to be approved.

Is it better to buy or rent?

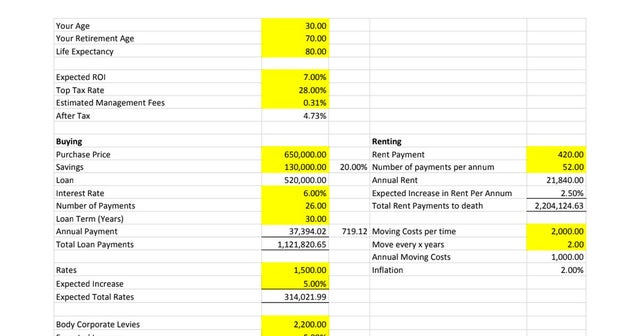

Renting is usually cheaper than buying a house. It is important to realize that renting is generally cheaper than buying a home. You will still need to pay utilities, repairs, and maintenance. A home purchase has many advantages. You'll have greater control over your living environment.

What flood insurance do I need?

Flood Insurance protects from flood-related damage. Flood insurance can protect your belongings as well as your mortgage payments. Find out more information on flood insurance.

What are the downsides to a fixed-rate loan?

Fixed-rate loans tend to carry higher initial costs than adjustable-rate mortgages. You may also lose a lot if your house is sold before the term ends.

Statistics

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

External Links

How To

How to locate an apartment

Moving to a new place is only the beginning. This takes planning and research. It involves research and planning, as well as researching neighborhoods and reading reviews. While there are many options, some methods are easier than others. Before renting an apartment, it is important to consider the following.

-

It is possible to gather data offline and online when researching neighborhoods. Online resources include Yelp. Zillow. Trulia. Realtor.com. Local newspapers, landlords or friends of neighbors are some other offline sources.

-

You can read reviews about the neighborhood you'd like to live. Yelp, TripAdvisor and Amazon provide detailed reviews of houses and apartments. Local newspaper articles can be found in the library.

-

Call the local residents to find out more about the area. Talk to those who have lived there. Ask them what they liked and didn't like about the place. Ask them if they have any recommendations on good places to live.

-

Consider the rent prices in the areas you're interested in. If you are concerned about how much you will spend on food, you might want to rent somewhere cheaper. Consider moving to a higher-end location if you expect to spend a lot money on entertainment.

-

Find out all you need to know about the apartment complex where you want to live. For example, how big is it? How much is it worth? Is it pet friendly What amenities do they offer? Are you able to park in the vicinity? Are there any rules for tenants?