Cash out refinances can be beneficial for people who are looking to make extra money to improve their credit scores. Cash out refinance requires a lower credit score than conventional mortgage loans. However, personal loans have higher closing costs. In addition, you may have to pay mortgage insurance, or PMI.

Rates are lower that credit cards

A cash-out refinance loan is a type that you can use the equity of your home to get cash. You can use the money to accomplish many things. These can include investing in property or saving for retirement. High interest debts can be paid off with a cash-out refinance. These debts can be paid off by using cash from a cash-out refinance. The money you withdraw can be used to pay for college tuition for your child. The refinance rate must not exceed the student loan's interest rate.

The home equity credit line of credit is another type of cash-out refinance. This type of loan lets you use the difference in your home's worth and your mortgage balance to repay your credit card debt. Many credit cards charge interest rates up to 30%. However, home equity loans have lower interest rates than credit cards. This means that you can save thousands of dollars over the course of your loan.

Personal loans come with higher closing costs than those for business loans.

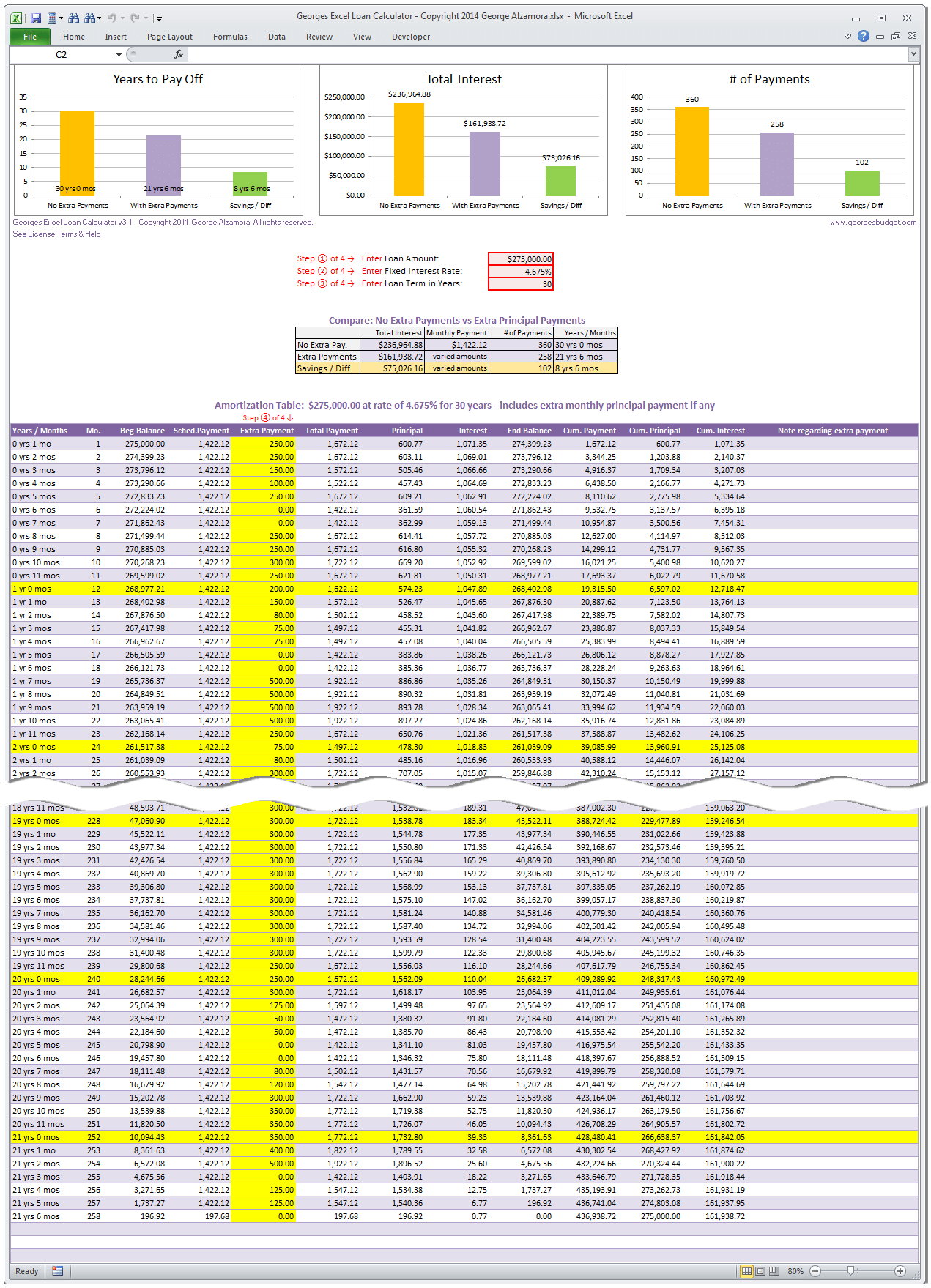

For a cash out refinance, closing costs are typically higher than for personal loans. Because the lender is taking on more risk with this type of loan, they charge higher closing costs. Add closing costs to the loan amount. The mortgage origination charge, usually around 1% of total loan amount, is the biggest closing cost. That translates into a $1,000 fee per $100,000 borrowed. Additional fees include an appraisal, credit check and title search.

Cash out refinances have a downside. They can take a lot of time. For those who have urgent cash needs, the underwriting process may take weeks. Based on your financial situation, the closing costs of a refinance cash out can run from $4,000 up to $10,000. Although this seems like a small sum, it will significantly impact the cash you receive upon closing.

You might be required to pay PMI

If you're not ready to pay a higher down payment or you're considering a cash out refinance, you may be required to pay private mortgage insurance. This type of insurance is designed to protect the lender in the event that you default on the loan. The insurance costs a monthly fee, which you pay together with your mortgage payment.

Before deciding whether to refinance your cash out loan, consider the cost and benefit of the loan. A cash out refinance can be a great tool to consolidate debt, or to fund home improvement projects. Before you decide if this loan is right for your needs, you need to know your financial goals.

The loan-to–value ratio is a factor in how much money can be borrowed for a cash-out refinance. A loan with a 5% down payment is typically considered low loan-to value ratio. You can avoid PMI on cash-out refinances with this lower ratio.

FAQ

Do I need flood insurance

Flood Insurance covers flooding-related damages. Flood insurance helps protect your belongings and your mortgage payments. Learn more information about flood insurance.

How do I calculate my interest rate?

Market conditions affect the rate of interest. In the last week, the average interest rate was 4.39%. Multiply the length of the loan by the interest rate to calculate the interest rate. Example: You finance $200,000 in 20 years, at 5% per month, and your interest rate is 0.05 x 20.1%. This equals ten bases points.

How can I determine if my home is worth it?

If your asking price is too low, it may be because you aren't pricing your home correctly. You may not get enough interest in the home if your asking price is lower than the market value. For more information on current market conditions, download our Home Value Report.

Is it possible to quickly sell a house?

If you have plans to move quickly, it might be possible for your house to be sold quickly. However, there are some things you need to keep in mind before doing so. First, you must find a buyer and make a contract. You must prepare your home for sale. Third, your property must be advertised. Finally, you should accept any offers made to your property.

Statistics

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

External Links

How To

How to Find Houses To Rent

Finding houses to rent is one of the most common tasks for people who want to move into new places. However, finding the right house may take some time. Many factors affect your decision-making process when choosing a home. These factors include price, location, size, number, amenities, and so forth.

To make sure you get the best possible deal, we recommend that you start looking for properties early. Also, ask your friends, family, landlords, real-estate agents, and property mangers for recommendations. You'll be able to select from many options.